The Consigliere

Seven years, $120 million, and why wealth management is built to move money, not grow it.

Six and a Half Minutes

It was about 11 in the morning in the summer of 2016, two months into my new post in Puerto Rico, when I understood what I had actually signed up for.

I was standing at my friend and colleague Eligio’s desk with an espresso, pretending to be there for the coffee. The machine was tucked in the corner of his cubicle, technically a safety hazard, an unauthorized electrical appliance in a regulated financial environment. We kept it anyway. Some battles aren’t worth fighting. Eligio had a cheerful disposition that made his corner of the office the natural place to land — always a laugh, always a bright take on whatever was going wrong that morning. I looked forward to that coffee almost every day.

The desk next to Eligio’s belonged to the Argentine. He was on a call. I heard the client’s name, a name the whole floor knew, and I stopped pretending.

The conversation started the way all his conversations started. Not with a pitch. Not with urgency. With warmth.

“How’s the wife? How are the kids? Good, good. Yes, I have the list ready.”

His voice on the phone was the same as his voice in person, unhurried, certain, the voice of someone who has never once worried that the other person might hang up. He read through the options one by one. Preferred stocks, mostly. High yield. Some barely investment grade, a few below. When he got to one that carried more risk than the rating suggested, I heard him say it:

“It’s a double B plus… Almost a triple B minus…”

I remember setting down my espresso.

Almost. The entire architecture of what he was doing lived in that one word. Not junk. Almost not junk. Close enough to safety that a client who trusted him wouldn’t ask the follow-up question. Far enough from safety that the yield was worth talking about.

I heard variations of this language constantly. “It’s almost investment grade” for bonds that were firmly junk. “It’s kind of like a treasury bond” for investment-grade corporate debt that had nothing to do with government-backed securities and could not be compared to one. These phrases traveled through the office like scripts — not lies exactly, but framings designed to make risk sound like proximity to safety. Every word of it was captured on a recorded line, as required by regulation. To this day, I don’t fully understand why none of it was flagged.

He went through twelve options. Then he paused.

“I think you should go with this one. Or this one.”

Twelve choices became two. The client picked one. I watched the Argentine’s expression change. Not dramatically, just a small shift, the satisfaction of a man whose Tuesday was going exactly as planned.

He read the transaction script from memory. Calm, methodical, every required disclosure in the right order. The recorded line captured all of it. The compliance box was checked.

The call lasted six and a half minutes.

He made $25,000 in commissions.

I picked up my espresso and walked back to my cubicle. I had been pleased with my morning. I was no longer pleased with my morning.

That was the job. Not managing money. Moving it.

The Office

I had arrived in Hato Rey about eight weeks earlier.

It was a Tuesday morning, just west of San Juan’s financial district, and the walk from the parking lot to the ground-floor entrance took maybe ninety seconds. I sweated through my entire shirt in that time. I was wearing a full suit, tie, the works, because I was 26 and I didn’t know any better, and I wanted to make an impression.

The air conditioning hit me at the door like a wall. That’s when I saw Eva for the first time. I’d worked with her for over half a year, coordinating from Caracas, and I only knew her by her professional and yet very sweet voice. Seeing a face attached to that voice was one of those quietly strange moments that offshore banking produces.

The office was not what the job title suggests. Private wealth management, Citibank Latin America: you picture mahogany and discretion. What I got was a ground-floor call center with good lighting. Cream cubicles in long rows. A single Bloomberg terminal at the end of the main walkway. Flat screens mounted across the walls, all tuned to CNBC, all on mute, the market ticker scrolling silently over footage of people talking about money. The hum of AC. Phones ringing. Conversations in Spanish, mostly Puerto Rican accents, a few Venezuelans in our corner.

Everyone was in khakis and a button-down. I was in a full suit.

I never made that mistake again.

This was not the office I had imagined. I had wanted Miami. New York. Floor-to-ceiling glass, a client lounge, the kind of address that signals you’ve arrived. What I got was a ground-floor call center in San Juan, Puerto Rico. But it beat Caracas during hyperinflation by a distance I couldn’t yet fully calculate. And I was already planning my first client visit to Miami, before I’d even set up my login.

I was 26, and so certain this was a stepping stone. I was treating a $120 million book of business like a rung on a ladder I was sure I’d keep climbing. Looking back, that was the arrogance of it. I knew I was lucky. I didn’t know how lucky I was.

Within a week, I had discovered the full range of my wireless headset. I was the only one in the office who walked while on calls, pacing the entire floor, weaving between cubicles, all the way to the ops door at the far corner of the building before the signal started breaking up. People shushed me as I went past. I told them I needed my steps. Both things were true. I’d been sitting at a desk in Caracas for three years and I was done with it. The walking was how I thought. The headset was what made it possible. I averaged over twelve thousand steps a day without ever leaving the building.

The operation had started as something elegant. Citibank’s Puerto Rico office was a wholly owned subsidiary, a registered broker-dealer paying Puerto Rico’s discounted corporate tax rate to house Latin American private wealth management. In its heyday, it had grown to tens of billions in assets under management across markets from Costa Rica to Argentina. By the time I started in 2012, the heyday was over. The bank was contracting, selling off businesses, reducing its Latin American footprint. The clients who remained, the most loyal, the most lucrative, had been consolidated into this ground-floor office in Hato Rey. Around thirty advisors. Dell and HP laptops that felt like $300 Best Buy specials. A contraband black Nespresso machine we kept hidden from compliance because it was technically a safety hazard.

Some battles aren’t worth fighting.

The office ran on a ranking system. Bi-weekly performance meetings. Every advisor measured by gross production: total commissions generated, regardless of portfolio size. Not return on investment. Not client outcomes. Gross dollars. It was Glengarry Glen Ross with headsets and Bloomberg terminals, and nobody wanted to be at the bottom of the list.

Carlos, Eligio’s assistant and my closest friend in Puerto Rico, sat nearby — the kind of person you detour past on the way to anywhere just because the conversation is always worth it. Between him, Eligio, and the machine, that corner of the office was where the day actually started.

It took me about eight weeks to understand that the most important person in that office was not the branch manager, not the senior advisors with the loudest voices, but a quiet Argentine in the back left corner who seemed, on most days, to be doing almost nothing at all.

He was the highest producer in the office. He barely moved.

What He Was Actually Selling

What I had just watched wasn’t exceptional. It was the business model.

Every office has a version of the Argentine. The highest producer is rarely the hardest worker. He is the one with the deepest relationships with clients who have a tendency to trade, and to trade often. The 80/20 rule applies to private banking the way it applies to every sales operation: 80% of revenue comes from 20% of clients. The art of the job, if there is one, is identifying which 20% and making sure they never stop calling.

This is the casino model. Casinos don’t make their money from casual tourists. They make it from the regulars — the people who come back, who know the dealers by name, who have convinced themselves that this time the pattern will hold. My colleague’s best client was that person. He wasn’t having his wealth managed. He was having his addiction managed. And my colleague, patient, warm, unhurried, never pushy, was the most effective kind of bookie: the kind who makes you feel like a valued partner rather than a revenue stream.

The commission grid doesn’t reward outcomes. It rewards transactions. Every trade pays. Doing nothing doesn’t. Activity is the product. Performance is the story told about it.

And then there were the trailer fees.

Mutual funds pay quarterly fees, called 12b-1 fees in regulatory language, to the broker-dealers and advisors who keep client money invested in them. The SEC defines them as fees paid from a fund’s own assets for distribution and marketing. In practice, they function as a recurring payment to the advisor for not moving the money. The SEC has brought dozens of enforcement actions against firms that failed to properly disclose this conflict of interest to clients. Most clients have no idea the arrangement exists.

My $120 million affluent book was roughly 70% mutual funds. That generated a reliable quarterly income stream regardless of how those funds actually performed. It was the closest thing to passive income the active management industry offers; the irony was not lost on me.

I want to be precise about what I did and didn’t do inside this system. I tracked the mutual funds I sold. I monitored their expense ratios and their performance against their benchmarks. I believed in what I recommended. But I also knew, with full clarity, that if I had done what I actually believed was right for my clients, built low-cost index ETF portfolios and held them, I would have been fired for low production. The commission grid didn’t compensate ETF transactions the same way. We weren’t incentivized to buy them. So I sold actively managed mutual funds I believed in, tracked them carefully, and lived with the structural contradiction.

Here is what the data says about the funds I was selling:

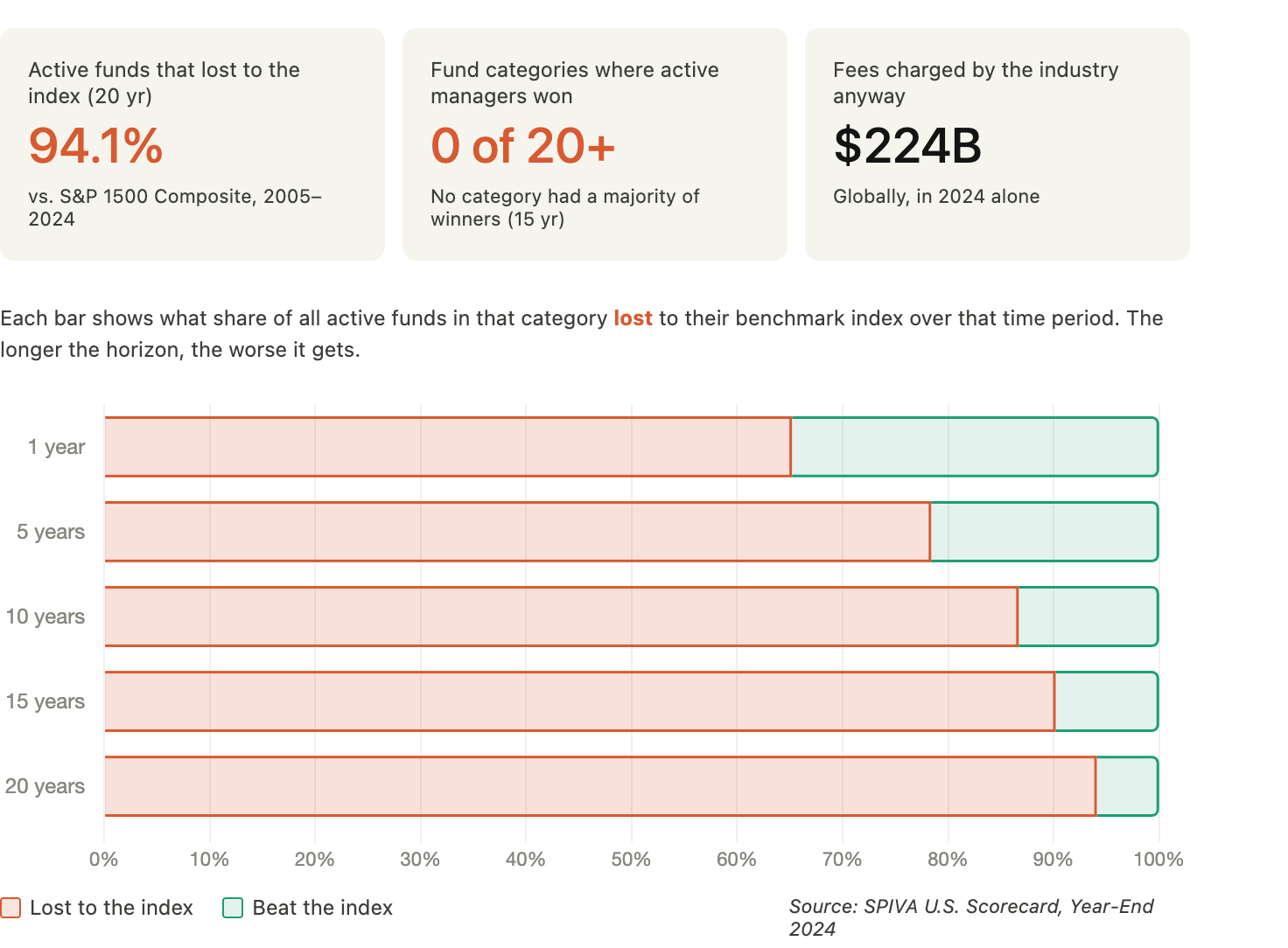

According to S&P Dow Jones Indices’ SPIVA Scorecard, the industry standard for measuring active versus passive performance published since 2002, over the 20-year period from 2005 to 2024, 94.1% of actively managed domestic funds underperformed the S&P 1500 Composite Index. Over the 15-year period ending December 2024, there were zero categories in which a majority of active managers outperformed their benchmark. Not one. And yet the industry generated $224 billion in fees globally in 2024.

That gap between what the industry produces and what it charges isn’t a failure of the system. It’s what the system is designed to produce.

Mr. F

Not every call was a transaction. Some clients just wanted to talk, a pen pal with a Bloomberg terminal, as I sometimes thought of it. Others came with specific ideas and wanted execution. Others were somewhere in between: a retired oil executive I’ll call Mr. F, colorful and sharp at 67, who treated his portfolio like a second career and called me every four to six weeks with fixed income plays he’d researched himself. We traded constantly. He became one of my best clients by volume alone.

One morning, he called with an ISIN or CUSIP number (unique identifiers for securities) and a request: a high-yield Latin American bond, high duration, the kind of instrument that pays well when it works and disappears when it doesn’t. $50,000. The commission would have been my morning done. I told him no. Not “I’d prefer you didn’t.” Not “here are the risks.” Just no. I can’t in good conscience recommend this. I told him it felt impulsive. That the yield was real, but so was the downside. He pushed back. We went back and forth. He ended up doing $10,000 instead of $50,000, unsolicited, with every disclaimer in place.

The bond filed for bankruptcy a few months later. He sold at thirty cents on the dollar.

He called me afterward. Not to complain. To change how we worked. After that, he would call with ideas and ask what I thought. If I didn’t agree, he wouldn’t move. The relationship went from transactional to a genuine partnership, built on a $7,000 loss I had tried to prevent.

That was the version of this job I loved. And it was always in tension with the version the commission grid was designed to produce.

The other side of that relationship was defense. Literally protecting clients from themselves. Years later, in the fourth quarter of 2018, the S&P dropped nearly 20%, its worst quarter in a decade. My phone started ringing before I’d finished my coffee. Clients who had never called to say the portfolio was up were suddenly calling to say: "Sell everything!”

Selling everything is almost always the wrong answer. But fear doesn’t respond to logic; it responds to the person on the other end of the phone. The research on this is consistent: as Scott Galloway has noted, the dopamine hit from winning money is significantly weaker than the pain of losing it. That asymmetry drives people toward decisions that destroy value. Sell at the bottom, miss the recovery, buy back in higher. You haven’t protected yourself. You’ve just converted a temporary loss into a permanent one.

Part of the job, a significant part, was stopping clients from doing that. Not because I always knew better, but because the presence of a trusted person on the phone created enough friction to interrupt the panic response. By the time we’d talked through it, the urgency had usually passed. The market recovered. The portfolio was fine. Nobody called to say thank you.

A robo-advisor executes. It doesn’t talk you down. The industry calls this ‘behavioral alpha’ — the measurable value of preventing panic selling. The concept is real. The fee structure built around it often isn’t.

The Annuity Debacle

Then there were the annuities. An annuity, as the SEC defines it, is a contract that converts a lump sum into a future income stream, a wealth transfer mechanism, not a growth vehicle. Advisors could earn up to 5% commission on the contract value at the point of sale. I never sold one to a client who didn’t already have one. Every annuity in my book I inherited from predecessors who sold them to clients who believed they were buying hedged-growth and fixed-income products. They weren’t. They were trading liquidity for an income schedule they often didn’t need, at a commission rate that made them among the most lucrative single transactions an advisor could execute. I managed those accounts carefully. I never added to them. But I understood exactly why they existed in the portfolios I inherited; it had nothing to do with what was best for the client.

CoCos

My first boss, Gino, arrived in my life during the fall of 2012 when I started at Citi. He was my direct manager until January 2014, when a restructuring at the bank ended his tenure after barely 15 months. But the impression he left lasted the rest of my career.

He was not a tall man, but he carried himself like someone who had never once needed to be. Athletic build, always in a suit, Tag Heuer glasses, hair perfectly combed. He had grown a beard by the time I really got to know him, reddish-tinted, which I mercilessly made fun of. He was a mentor in the way that the best mentors are: he didn’t try to make me more like him, he tried to make me better at being myself.

He also beat the arrogance out of me, which I needed more than I knew. I arrived at that office, certain I understood markets. Gino was the first person to show me what I actually didn’t know — inflation hedging, the mechanics of currency controls, how to use debt as a shield against a depreciating currency. These were Venezuelan realities I had lived but never fully understood as systems. He understood them as systems. I owe him more than I’ve ever told him.

One evening, about a month into my tenure, we were working late. The investment product committee had asked for presentations from each country team: best practices, what was selling, and what risks had been identified. We had discovered that advisors across our Latin American portfolios had been buying contingent convertible bonds, ‘CoCos’, in significant size. High yields, 7% to 8% interest rates, selling like hotcakes. The commission grid made them irresistible. A CoCo paid advisors 3% to 3.5% at the point of sale. A 30-year U.S. Treasury — the benchmark for safety — paid a maximum of 1.5%. An investment-grade corporate bond of similar maturity paid around 2%. The math wasn’t subtle. Higher risk, longer duration, higher commission. Clients got yield. Advisors got paid. Nobody read the prospectus. CoCos are bonds that convert to equity, potentially worthless equity, if certain liquidity covenants are triggered. Our clients thought they owned senior fixed-income notes. Under specific conditions, they owned preferred shares that could be wiped out.

It was 7:30 pm, and Gino was exasperated. Millions of dollars in our Venezuelan portfolio were tied to these securities. If any of them triggered, clients could sue for being misled. I remember him looking at the Bloomberg terminal and saying: “How can you sell something without reading what you’re selling?”

That’s when he said it. Not in a training session, not in a formal speech, but in the middle of a compliance emergency, tired, genuinely troubled by what we’d found. He said: “You can make a lot of money in this business, but it has to be done the right way. Because money is the third most intimate thing in a person’s life, after family and health. You can’t do the other two without managing the third correctly.”

That was the version of the job I had signed up for. Not a salesman. A consigliere — the person who translated the bank's cold machinery into something a family could actually use.

He believed that. I believed that. The system we operated within made it structurally difficult to act on.

The Compliance Trap

By the time I joined Citi in 2012, we were already midway through a consent order with the Office of the Comptroller of the Currency, a formal regulatory intervention citing deficiencies in our BSA/AML compliance program. We were prohibited from opening new accounts. Six years later, the OCC assessed Citibank a $70 million civil money penalty for still not being in compliance. This was the environment I was operating in.

The burden fell almost entirely on the wrong people.

I managed an account for a client and his family. About $300,000, legitimate savings, no red flags. His wife’s father passed away in Switzerland, and she was set to inherit approximately $3 million from a family trust. That windfall became the starting point of a fourteen-month compliance odyssey.

I reported the incoming funds to my compliance officer immediately. She gave me a list of documentation needed to establish source of wealth. The client provided trust documents, articles of incorporation, financial statements. It came back insufficient. Over the next fourteen months, I became a forensic accountant. I tracked down property deeds and defunct company registrations in Venezuela. I found share certificates for companies that had only ever traded on the Venezuelan stock exchange. I ran inflation calculations, converting bolivars to dollars across years of devaluation, to prove that a dead man’s legitimate career had produced the wealth his daughter was inheriting.

I knew these people. They were not money launderers. They were a family whose patriarch had spent forty years building something, who had the misfortune of holding it in a Swiss trust when the U.S. regulatory environment decided that Venezuelan wealth was, by definition, suspicious. The corrupt politicians, the ones actually laundering money, were doing it through the Isle of Man, through Andorra, through Swiss private banks that the ICIJ’s FinCEN Files investigation later documented processing hundreds of millions in Venezuelan state funds through shell companies. Those flows went through entirely different channels. My retired clients with Swiss trusts were the ones who spent 14 months on paperwork and multiple account freezes.

The industry’s response was to exit. Wells Fargo abandoned the offshore wealth management market entirely. According to American Banker, top U.S. banks cut correspondent lines across Latin America by roughly 50% after 2013. The clients who lost access to banking weren’t the corrupt ones. The corrupt ones had already found other arrangements.

As for my own group, in 2022, Citi sold its International Personal Bank business in Puerto Rico and Uruguay to Insigneo. The operation I spent seven years building no longer exists under that name. The machine found other arrangements too.

By my final years, I was spending more time proving my clients weren’t criminals than actually serving them. That was the nail in the coffin.

What I Do With My Own Money

After seven years inside the system, I stopped trying to beat it.

After managing $120 million for 450 clients, after understanding commission grids, trailer fees, annuities, and compliance burdens from the inside, here is what I do with my own money.

I keep it in two positions: the Vanguard S&P 500 ETF (VOO) and the Invesco NASDAQ 100 ETF (QQQM). Blended expense ratio of 0.09%. No advisor. No quarterly calls. No list of twelve narrowed to two.

If you’re going to use an advisor — and there are legitimate reasons to, particularly for estate planning, tax efficiency, or if you need someone to talk you off the ledge in a correction — ask one question before anything else: how do you get paid? If the answer is commissions, the incentive structure I described above applies to every conversation you’ll have. The advisor is not your enemy, but the grid is not your friend. A fee-based account, where the advisor charges a flat percentage of assets under management regardless of trading activity, aligns the incentives far better. When your portfolio grows, they earn more. When it shrinks, they earn less. That’s the relationship the commission model structurally prevents.

The tradeoff is control. Fee-based advisors often have discretion to make investment decisions without calling you first. Some clients find that liberating. Others hate it. If you want to approve every trade, you may end up back on a commission structure — just go in knowing what that means for the conversation you’re having.

Over twelve years, these positions have outperformed almost every individual stock pick I’ve made, with very few exceptions, and they’ve been mostly luck, not craft. The compounding math is not complicated, but it is relentless.

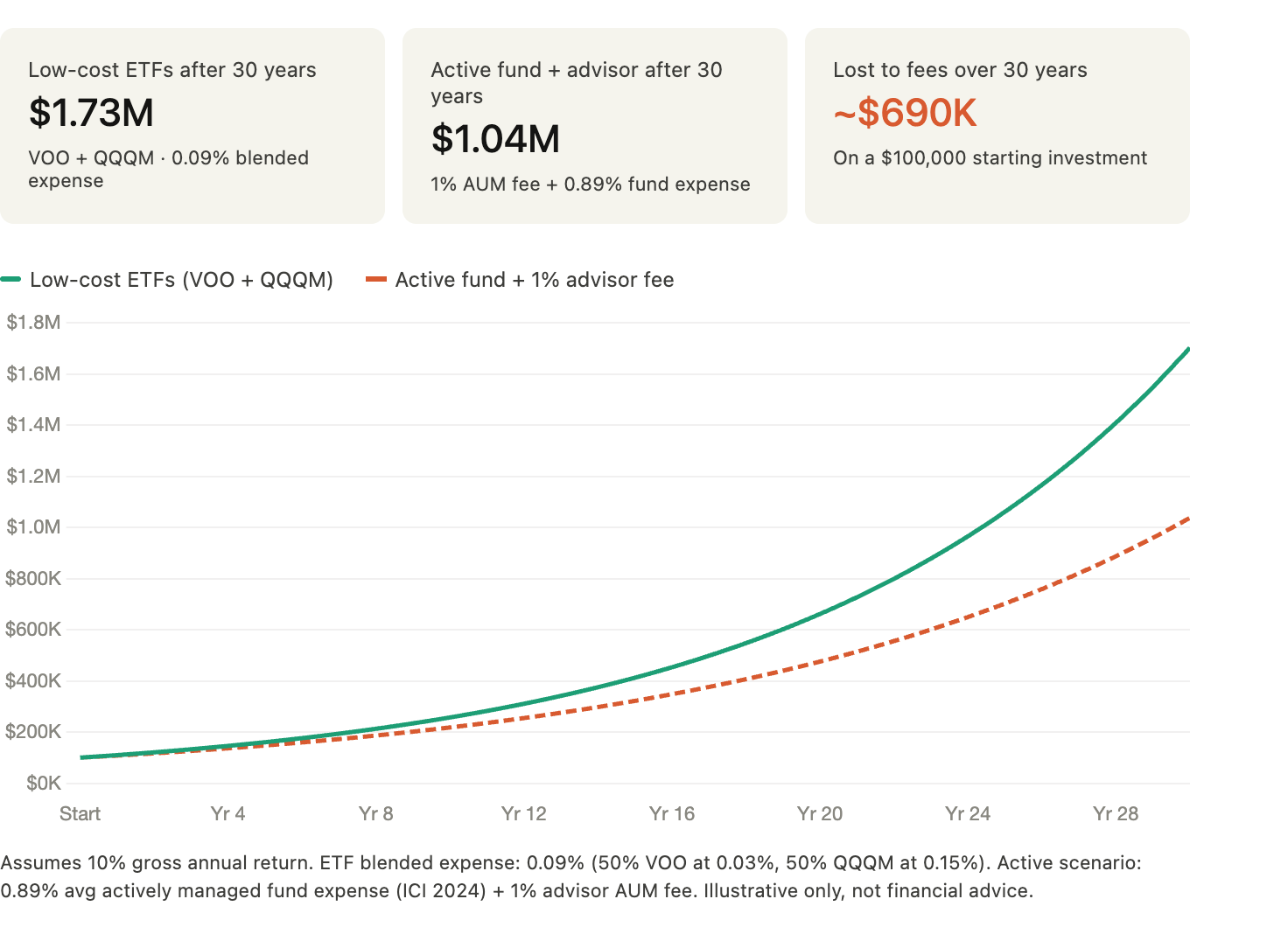

On a $100,000 starting investment, the difference between a 0.09% blended expense ratio and the 1.89% total cost of a typical actively managed fund plus advisor fee — compounded over 30 years at a 10% gross annual return — is approximately $690,000. Not in returns. In fees. Money that leaves your portfolio quietly, every year, regardless of performance.

That is what financial literacy costs when you don’t have it. And that is what the industry is built on.

I’m not your financial advisor. I’m someone who spent seven years inside the machine and then spent the next decade watching the index funds outperform everything I used to sell. Draw your own conclusions.

The Last Day

I gave a week’s notice.

I kept it quiet for as long as I could. In private banking, when you announce you’re leaving, the clock starts on your book. Accounts get reassigned. Relationships you spent years building get handed to someone else before you’ve finished clearing your desk. So I told almost no one until I had to.

The last day was a Thursday. San Juan in the morning: the usual ten-minute shower that comes out of nowhere and then disappears, leaving the air humid and warm and smelling like wet concrete and salt. I drove to Hato Rey in a suit, not because I needed to, but because it felt right. The same way I had arrived.

I went around the entire floor. Luis, my friend, who had let me in on my first day. Eva, my wonderful assistant, who had made my entire operation run, and who cried when I told her my plans months ago. My colleagues in the Venezuelan corner. The trading desk. The operations team. Even my compliance officer, with whom I had a relationship that was equal parts gratitude and frustration. Even my boss’s boss, with whom things had been complicated, who looked at me across his desk and said: “I wish I could have done what you’re doing twenty years ago.”

I thought about that for a long time afterward.

I returned my laptop. I left my wireless headset on its charging station, the one that had taken me all the way to the ops door and back, ten thousand steps a day, for years. I handed in my key card. I picked up the box.

450 accounts. $120 million in AUM. Running like the Japanese rail system. Built from hand-me-down portfolios nobody wanted, inherited at 26, managed with everything I had. Every client called. Every position tracked. Every expense ratio monitored. And none of that — not one basis point of it — was what the grid measured. I was proud of it. I was also done with it.

I walked out through the glass door, past the Citi logo, into the parking lot. The moving truck was coming on Friday. Then off to Washington DC on Saturday, and a new chapter on Monday — Business School.

Behind me, through the glass, I could hear it.

The phones. Still going. Everyone still on their headsets, still pitching, still executing, still closing. As if nothing had happened. As if I had never been there at all.

Somewhere in the back left corner of the floor, I knew, the Argentine was at his desk.

Waiting for the phone to ring.

Waiting for the next six and a half minutes.